Renewable energy commercialization

| Renewable energy |

|---|

|

Biofuel |

Renewable energy commercialization involves the diffusion of three generations of renewable energy technologies dating back more than 100 years. First-generation technologies, which are already mature and economically competitive, include biomass, hydroelectricity, geothermal power and heat. Second-generation technologies are market-ready and are being deployed at the present time; they include solar heating, photovoltaics, wind power, solar thermal power stations, and modern forms of bioenergy. Third-generation technologies require continued R&D efforts in order to make large contributions on a global scale and include advanced biomass gasification, biorefinery technologies, hot-dry-rock geothermal power, and ocean energy.[2][3]

There are many non-technical barriers to the widespread use of renewables,[4][5] and it is mainly public policy and political leadership that are driving the widespread acceptance of renewable energy technologies.[6] Some 85 countries now have targets for their own renewable energy futures, and have enacted wide-ranging public policies to promote renewables.[7][8] Climate change concerns[5][9][10] are driving increasing growth in the renewable energy industries.[11][12][13] Leading renewable energy companies include First Solar, Gamesa, GE Energy, Q-Cells, Sharp Solar, Siemens, SunOpta, Suntech, and Vestas.[14][15][16]

Global revenues for solar photovoltaics, wind power, and biofuels expanded from $76 billion in 2007 to $115 billion in 2008. New global investments in clean energy technologies—including venture capital, project finance, public markets, and research and development—expanded by 4.7 percent from $148 billion in 2007 to $155 billion in 2008.[17] Continued growth for the renewable energy sector is expected and promotional policies helped the industry weather the 2009 economic crisis better than many other sectors.[17] U.S. President Barack Obama's American Recovery and Reinvestment Act of 2009 included more than $70 billion in direct spending and tax credits for clean energy and associated transportation programs. Clean Edge suggests that the commercialization of clean energy has helped countries around the world pull out of the 2009 global financial crisis.[17] Globally, there are an estimated 3 million direct jobs in renewable energy industries, with about half of them in the biofuels industry.[18]

Overview

Rationale for renewables

Renewable energy technologies are essential contributors to the energy supply portfolio, as they contribute to world energy security, reduce dependency on fossil fuels, and provide opportunities for mitigating greenhouse gases.[2] Climate-disrupting fossil fuels are being replaced by clean, climate-stabilizing, non-depletable sources of energy:

...the transition from coal, oil, and gas to wind, solar, and geothermal energy is well under way. In the old economy, energy was produced by burning something — oil, coal, or natural gas — leading to the carbon emissions that have come to define our economy. The new energy economy harnesses the energy in wind, the energy coming from the sun, and heat from within the earth itself.[19]

The International Energy Agency estimates that nearly 50% of global electricity supplies will need to come from renewable energy sources in order to halve carbon dioxide emissions by 2050 and minimise significant, irreversible climate change impacts.[5]

Three generations of technologies

The term renewable energy covers a number of sources and technologies at different stages of commercialization. The International Energy Agency (IEA) has defined three generations of renewable energy technologies, reaching back over 100 years:

- First-generation technologies emerged from the industrial revolution at the end of the 19th century and include hydropower, biomass combustion, geothermal power and heat. These technologies are quite widely used.[2]

- Second-generation technologies include solar heating and cooling, wind power, modern forms of bioenergy, and solar photovoltaics. These are now entering markets as a result of research, development and demonstration (RD&D) investments since the 1980s. Initial investment was prompted by energy security concerns linked to the oil crises of the 1970s but the enduring appeal of these technologies is due, at least in part, to environmental benefits. Many of the technologies reflect significant advancements in materials.[2]

- Third-generation technologies are still under development and include advanced biomass gasification, biorefinery technologies, concentrating solar thermal power, hot-dry-rock geothermal power, and ocean energy. Advances in nanotechnology may also play a major role.[2]

First-generation technologies are well established, second-generation technologies are entering markets, and third-generation technologies heavily depend on long-term RD&D commitments, where the public sector has a role to play.[2]

Recent growth of renewables

During the five-years from the end of 2004 through 2009, worldwide renewable energy capacity grew at rates of 10–60 percent annually for many technologies. For wind power and many other renewable technologies, growth accelerated in 2009 relative to the previous four years.[20] More wind power capacity was added during 2009 than any other renewable technology. However, grid-connected PV increased the fastest of all renewables technologies, with a 60 percent annual average growth rate for the five-year period.[20]

| Selected global indicators | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 |

|---|---|---|---|---|---|---|

| Investment in new renewable capacity (annual) | 30 | 38 | 63 | 104 | 130 | 150 billion USD |

| Existing renewables power capacity, including large-scale hydro |

895 | 930 | 1,020 | 1,070 | 1,140 | 1,230 GWe |

| Existing renewables power capacity, excluding large hydro |

160 | 182 | 207 | 240 | 280 | 305 GWe |

| Wind power capacity (existing) | 48 | 59 | 74 | 94 | 121 | 159 GWe |

| Solar PV capacity (grid-connected) | 7.6 | 13.5 | 21 GWe | |||

| Solar hot water capacity | 77 | 88 | 105 | 126 | 149 | 180 GWth |

| Ethanol production (annual) | 30.5 | 33 | 39 | 50 | 69 | 76 billion liters |

| Biodiesel production (annual) | 10 | 15 | 17 billion liters | |||

| Countries with policy targets for renewable energy use |

45 | 49 | 68 | 75 | 85 |

In 2008 for the first time, more renewable energy than conventional power capacity was added in both the European Union and United States, demonstrating a "fundamental transition" of the world's energy markets towards renewables, according to a report released by REN21, a global renewable energy policy network based in Paris.[22]

A 2010 survey conducted by Applied Materials shows that two-thirds of Americans believe solar technology should play a greater role in meeting the country's energy needs. In addition, "three-quarters of Americans feel that increasing renewable energy and decreasing U.S. dependence on foreign oil are the country's top energy priorities". According to the survey, "67 percent of Americans would be willing to pay more for their monthly utility bill if their utility company increased its use of renewable energy".[23]

Economic trends

The International Solar Energy Society argues that renewable energy technologies and economics will improve with time, and that they are "sufficiently advanced at present to allow for major penetrations of renewable energy into the mainstream energy and societal infrastructures".[24] Indicative, levelised, economic costs for renewable power (exclusive of subsidies or policy incentives) are shown in the Table below.

| Power generator | Typical characteristics | Typical electricity costs (U.S. cents/kWh) |

|---|---|---|

| Large hydro | Plant size: 10 - 18,000 MW | 3-5 |

| Small hydro | Plant size: 1-10 MW | 5-12 |

| Onshore wind | Turbine size: 1.5 - 3.5 MW | 5-9 |

| Offshore wind | Turbine size: 1.5 - 5 MW | 10-14 |

| Biomass power | Plant size: 1-20 MW | 5-12 |

| Geothermal power | Plant size: 1-100 MW | 4-7 |

| Rooftop solar PV | Peak capacity: 2-5 kilowatts-peak | 20-50 |

| Utility-scale solar PV | Peak capacity: 200 kW to 100MW | 15-30 |

| Concentrating solar thermal power (CSP) | 50-500 MW trough | 14-18 |

As time progresses, renewable energy generally gets cheaper,[25][26] while fossil fuels generally get more expensive. Al Gore has explained that renewable energy technologies are declining in price for three main reasons:[27]

First, once the renewable infrastructure is built, the fuel is free forever. Unlike carbon-based fuels, the wind and the sun and the earth itself provide fuel that is free, in amounts that are effectively limitless.

Second, while fossil fuel technologies are more mature, renewable energy technologies are being rapidly improved. So innovation and ingenuity give us the ability to constantly increase the efficiency of renewable energy and continually reduce its cost.

Third, once the world makes a clear commitment to shifting toward renewable energy, the volume of production will itself sharply reduce the cost of each windmill and each solar panel, while adding yet more incentives for additional research and development to further speed up the innovation process.[27]

First-generation technologies

First-generation technologies are widely used in locations with abundant resources. Their future use depends on the exploration of the remaining resource potential, particularly in developing countries, and on overcoming challenges related to the environment and social acceptance.

Biomass

Biomass for heat and power is a fully mature technology which offers a ready disposal mechanism for municipal, agricultural, and industrial organic wastes. However, the industry has remained relatively stagnant over the decade to 2007, even though demand for biomass (mostly wood) continues to grow in many developing countries. One of the problems of biomass is that material directly combusted in cook stoves produces pollutants, leading to severe health and environmental consequences, although improved cook stove programmes are alleviating some of these effects. First-generation biomass technologies can be economically competitive, but may still require deployment support to overcome public acceptance and small-scale issues.[2]

Hydroelectricity

Hydroelectric plants have the advantage of being long-lived and many existing plants have operated for more than 100 years. Hydropower is also an extremely flexible technology from the perspective of power grid operation. Large hydropower provides one of the lowest cost options in today’s energy market, even compared to fossil fuels and there are no harmful emissions associated with plant operation.[2]

Hydroelectric power is currently the world’s largest installed renewable source of electricity, supplying about 17% of total electricity in 2005.[28] China is the world's largest producer of hydroelectricity in the world, followed by Canada.

However, there are several significant social and environmental disadvantages of large-scale hydroelectric power systems: dislocation of people living where the reservoirs are planned, release of significant amounts of carbon dioxide and methane during construction and flooding of the reservoir, and disruption of aquatic ecosystems and birdlife.[29] Hydroelectric power is now more difficult to site in developed nations because most major sites within these nations are either already being exploited or may be unavailable for these environmental reasons. The areas of greatest hydroelectric growth are the growing economies of Asia. India and China are the development leaders; however, other Asian nations are also expanding hydropower.

There is a strong consensus now that countries should adopt an integrated approach towards managing water resources, which would involve planning hydropower development in co-operation with other water-using sectors.[2]

Geothermal power and heat

Geothermal power plants can operate 24 hours per day, providing baseload capacity. Estimates for the world potential capacity for geothermal power generation vary widely, ranging from 40 GW by 2020 to as much as 6,000 GW.[30][31]

Geothermal power capacity grew from around 1 GW in 1975 to almost 10 GW in 2008.[31] The United States is the world leader in terms of installed capacity, representing 3.1 GW. Other countries with significant installed capacity include the Philippines (1.9 GW), Indonesia (1.2 GW), Mexico (1.0 GW), Italy (0.8 GW), Iceland (0.6 GW), Japan (0.5 GW), and New Zealand (0.5 GW).[31][32] In some countries, geothermal power accounts for a significant share of the total electricity supply, such as in the Philippines, where geothermal represented 17 percent of the total power mix at the end of 2008.[33]

Geothermal (ground source) heat pumps represented an estimated 30 GWth of installed capacity at the end of 2008, with other direct uses of geothermal heat (i.e., for space heating, agricultural drying and other uses) reaching an estimated 15 GWth. As of 2008, at least 76 countries use direct geothermal energy in some form.[34]

Second-generation technologies

Markets for second-generation technologies have been strong and growing over the past decade, and these technologies have gone from being a passion for the dedicated few to a major economic sector in countries such as Germany, Spain, the United States, and Japan. Many large industrial companies and financial institutions are involved and the challenge is to broaden the market base for continued growth worldwide.[2][9]

Solar Heating

Solar heating systems are a well known second-generation technology and generally consist of solar thermal collectors, a fluid system to move the heat from the collector to its point of usage, and a reservoir or tank for heat storage. The systems may be used to heat domestic hot water, swimming pools, or homes and businesses. The heat can also be used for industrial process applications or as an energy input for other uses such as cooling equipment.[35]

In many warmer climates, a solar heating system can provide a very high percentage (50 to 75%) of domestic hot water energy. As of 2009, China has 27 million rooftop solar water heaters.[36]

Photovoltaics

Photovoltaic (PV) cells, also called solar cells, convert light into electricity. In the 1980s and early 1990s, most photovoltaic modules were used to provide remote-area power supply, but from around 1995, industry efforts have focused increasingly on developing building integrated photovoltaics and photovoltaic power stations for grid connected applications.

As of October 2009, the largest photovoltaic (PV) power plants in the world are the Olmedilla Photovoltaic Park (Spain, 60 MW), the Puertollano Photovoltaic Park (Spain, 50 MW), the Moura photovoltaic power station (Portugal, 46 MW), and the Waldpolenz Solar Park (Germany, 40 MW).[37] The largest photovoltaic power plant in North America is the 25 MW DeSoto Next Generation Solar Energy Center in Florida. The plant consists of over 90,000 solar panels.[38]

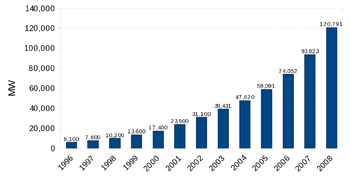

At the end of 2008, the cumulative global PV installations reached 15,200 MW.[8] Photovoltaic production has been doubling every two years, increasing by an average of 48 percent each year since 2002, making it the world’s fastest-growing energy technology. The top five photovoltaic producing countries are Japan, China, Germany, Taiwan, and the USA.[39]

Wind power

Some of the second-generation renewables, such as wind power, have high potential and have already realised relatively low production costs.[40][41] At the end of 2009, worldwide wind farm capacity was 157,900 MW, representing an increase of 31 percent during the year,[42] and wind power supplied some 1.3% of global electricity consumption.[43] Wind power is widely used in European countries, and more recently in the United States and Asia.[44][45] Wind power accounts for approximately 19% of electricity generation in Denmark, 11% in Spain and Portugal, and 9% in the Republic of Ireland.[46] These are some of the largest wind farms in the world, as of July 2010:

| Wind farm | Installed capacity (MW) |

Country |

|---|---|---|

| Capricorn Ridge Wind Farm | 662 | USA |

| Fowler Ridge Wind Farm | 750 | USA |

| Horse Hollow Wind Energy Center | 736 | USA |

| Roscoe Wind Farm | 781 | USA |

| San Gorgonio Pass Wind Farm | 619 | USA |

| Tehachapi Pass Wind Farm | 690 | USA |

Solar thermal power stations

Solar thermal power stations include the 354 MW Solar Energy Generating Systems power complex in the USA, Nevada Solar One (USA, 64 MW), Andasol 1 (Spain, 50 MW) and the PS10 solar power tower (Spain, 11 MW). Many other plants are under construction or planned, mainly in Spain and the USA.[47] In developing countries, three World Bank projects for integrated solar thermal/combined-cycle gas-turbine power plants in Egypt, Mexico, and Morocco have been approved.[47]

Modern forms of Bioenergy

Global ethanol production for transport fuel tripled between 2000 and 2007 from 17 billion to more than 52 billion litres, while biodiesel expanded more than ten-fold from less than 1 billion to almost 11 billion litres. Biofuels provide 1.8% of the world’s transport fuel and recent estimates indicate a continued high growth. The main producing countries for transport biofuels are the USA, Brazil, and the EU.[48]

Brazil has one of the largest renewable energy programs in the world, involving production of ethanol fuel from sugar cane, and ethanol now provides 18 percent of the country's automotive fuel. As a result of this and the exploitation of domestic deep water oil sources, Brazil, which for years had to import a large share of the petroleum needed for domestic consumption, recently reached complete self-sufficiency in liquid fuels.[49][50]

Nearly all the gasoline sold in the United States today is mixed with 10 percent ethanol, a mix known as E10,[51] and motor vehicle manufacturers already produce vehicles designed to run on much higher ethanol blends. Ford, DaimlerChrysler, and GM are among the automobile companies that sell flexible-fuel cars, trucks, and minivans that can use gasoline and ethanol blends ranging from pure gasoline up to 85% ethanol (E85). By mid-2006, there were approximately six million E85-compatible vehicles on U.S. roads.[52] The challenge is to expand the market for biofuels beyond the farm states where they have been most popular to date. Flex-fuel vehicles are assisting in this transition because they allow drivers to choose different fuels based on price and availability. The Energy Policy Act of 2005, which calls for 7.5 billion gallons of biofuels to be used annually by 2012, will also help to expand the market.[52]

The growing ethanol and biodiesel industries are providing jobs in plant construction, operations, and maintenance, mostly in rural communities. According to the Renewable Fuels Association, the ethanol industry created almost 154,000 U.S. jobs in 2005 alone, boosting household income by $5.7 billion. It also contributed about $3.5 billion in tax revenues at the local, state, and federal levels.[52]

Third-generation technologies

Third-generation renewable energy technologies are still under development and include advanced biomass gasification, biorefinery technologies, hot-dry-rock geothermal power, and ocean energy.[2] Third-generation technologies are not yet widely demonstrated or have limited commercialization. Many are on the horizon and may have potential comparable to other renewable energy technologies, but still depend on attracting sufficient attention and RD&D funding.[2]

New bioenergy technologies

According to the International Energy Agency, cellulosic ethanol biorefineries could allow biofuels to play a much bigger role in the future than organizations such as the IEA previously thought.[53] Cellulosic ethanol can be made from plant matter composed primarily of inedible cellulose fibers that form the stems and branches of most plants. Crop residues (such as corn stalks, wheat straw and rice straw), wood waste, and municipal solid waste are potential sources of cellulosic biomass. Dedicated energy crops, such as switchgrass, are also promising cellulose sources that can be sustainably produced in many regions of the United States.[54]

| Company | Location | Feedstock |

|---|---|---|

| Abengoa Bioenergy | Hugoton, KS | Wheat straw |

| BlueFire Ethanol | Irvine, CA | Multiple sources |

| Gulf Coast Energy | Mossy Head, FL | Wood waste |

| Mascoma | Lansing, MI | Wood |

| POET LLC | Emmetsburg, IA | Corn cobs |

| Range Fuels[57] | Treutlen County, GA | Wood waste |

| SunOpta | Little Falls, MN | Wood chips |

| Xethanol | Auburndale, FL | Citrus peels |

Ocean energy

First proposed more than thirty years ago, systems to harvest utility-scale electrical power from ocean waves have recently been gaining momentum as a viable technology. The potential for this technology is considered promising, especially on west-facing coasts with latitudes between 40 and 60 degrees:[58]

In the United Kingdom, for example, the Carbon Trust recently estimated the extent of the economically viable offshore resource at 55 TWh per year, about 14% of current national demand. Across Europe, the technologically achievable resource has been estimated to be at least 280 TWh per year. In 2003, the U.S. Electric Power Research Institute (EPRI) estimated the viable resource in the United States at 255 TWh per year (6% of demand).[58]

Funding for a wave farm in Scotland was announced in February 2007 by the Scottish Executive, at a cost of over 4 million pounds, as part of a £13 million funding packages for ocean power in Scotland. The farm will be the world's largest with a capacity of 3 MW generated by four Pelamis machines.[59]

The world's first commercial tidal power station was installed in 2007 in the narrows of Strangford Lough in Ireland. The 1.2 megawatt underwater tidal electricity generator, part of Northern Ireland's Environment & Renewable Energy Fund scheme, takes advantage of the fast tidal flow (up to 4 metres per second) in the lough. Although the generator is powerful enough to power a thousand homes, the turbine has minimal environmental impact, as it is almost entirely submerged, and the rotors pose no danger to wildlife as they turn quite slowly.[60]

Enhanced geothermal systems

As of 2008, geothermal power development was under way in more than 40 countries, partially attributable to the development of new technologies, such as Enhanced Geothermal Systems.[34] The development of binary cycle power plants and improvements in drilling and extraction technology may enable enhanced geothermal systems over a much greater geographical range than "traditional" Geothermal systems. Demonstration EGS projects are operational in the USA, Australia, Germany, France, and The United Kingdom.[61]

Nanotechnology thin-film solar panels

Solar power panels that use nanotechnology, which can create circuits out of individual silicon molecules, may cost half as much as traditional photovoltaic cells, according to executives and investors involved in developing the products. Nanosolar has secured more than $100 million from investors to build a factory for nanotechnology thin-film solar panels. The company expects the factory to open in 2010 and produce enough solar cells each year to generate 430 megawatts of power.

Renewable energy industry

Global revenues for solar photovoltaics, wind power, and biofuels expanded from $76 billion in 2007 to $115 billion in 2008. New global investments in clean energy technologies — including venture capital, project finance, public markets, and research and development — expanded by 4.7 percent from $148 billion in 2007 to $155 billion in 2008.[17]

Wind power companies

Vestas is the largest wind turbine manufacturer in the world with a 20% market share in 2008.[16] The company operates plants in Denmark, Germany, India, Italy, Britain, Spain, Sweden, Norway, Australia and China,[62] and employs more than 20,000 people globally.[63] After a sales slump in 2005, Vestas recovered and was voted Top Green Company of 2006.[64] Vestas announced a major expansion of its North American headquarters in Portland, Oregon in December, 2008.[65]

GE Energy was the world's second largest wind turbine manufacturer in 2008, with 19% market share.[16] The company has installed over 5,500 wind turbines and 3,600 hydro turbines, and its installed capacity of renewable energy worldwide exceeds 160,000 MW.[66] GE Energy bought out Enron Wind in 2002 and also has nuclear energy operations in its portfolio.[67]

Gamesa, founded in 1976 with headquarters in Vitoria, Spain, was the world's third largest wind turbine manufacturer in 2008,[16] and it is also a major builder of wind farms. Gamesa’s main markets are within Europe, the US and China.

Other major wind power companies include Siemens, Suzlon, Sinovel and Goldwind.[16]

Photovoltaic companies

First Solar became the world's largest solar cell maker in 2009, producing some 1,100 MW of product, with a 13% market share. Suntech was in second place with production of 595 MW in 2009 and market share of 7%.[15] Sharp was close behind the leaders with 580 MW of output. Q-Cells and its 540 MW output was fourth in 2009. Yingli Green Energy, JA Solar Holdings, SunPower, Kyocera, Motech Solar and Gintech rounded out the 2009 Top 10 ranking.[15]

Non-technical barriers to acceptance

Newer and cleaner technologies may offer social and environmental benefits, but utility operators often reject renewable resources because they are trained to think only in terms of big, conventional power plants.[68] Consumers often ignore renewable power systems because they are not given accurate price signals about electricity consumption. Intentional market distortions (such as subsidies), and unintentional market distortions (such as split incentives) may work against renewables.[68] Benjamin K. Sovacool has argued that "some of the most surreptitious, yet powerful, impediments facing renewable energy and energy efficiency in the United States are more about culture and institutions than engineering and science".[69]

The obstacles to the widespread commercialization of renewable energy technologies are primarily political, not technical,[70] and there have been many studies which have identified a range of "non-technical barriers" to renewable energy use.[5][4][71] These barriers are impediments which put renewable energy at a marketing, institutional, or policy disadvantage relative to other forms of energy. Key barriers include:[4][71]

- Lack of government policy support, which includes the lack of policies and regulations supporting deployment of renewable energy technologies and the presence of policies and regulations hindering renewable energy development and supporting conventional energy development. Examples include subsidies for fossil-fuels, insufficient consumer-based renewable energy incentives, government underwriting for nuclear plant accidents, and complex zoning and permitting processes for renewable energy.

- Lack of information dissemination and consumer awareness.

- Higher capital cost of renewable energy technologies compared with conventional energy technologies.

- Difficulty overcoming established energy systems, which includes difficulty introducing innovative energy systems, particularly for distributed generation such as photovoltaics, because of technological lock-in, electricity markets designed for centralized power plants, and market control by established operators. As the Stern Review on the Economics of Climate Change points out:

- National grids are usually tailored towards the operation of centralised power plants and thus favour their performance. Technologies that do not easily fit into these networks may struggle to enter the market, even if the technology itself is commercially viable. This applies to distributed generation as most grids are not suited to receive electricity from many small sources. Large-scale renewables may also encounter problems if they are sited in areas far from existing grids.[72]

- Inadequate financing options for renewable energy projects, including insufficient access to affordable financing for project developers, entrepreneurs and consumers.

- Imperfect capital markets, which includes failure to internalize all costs of conventional energy (e.g., effects of air pollution, risk of supply disruption)[73] and failure to internalize all benefits of renewable energy (e.g., cleaner air, energy security).

- Inadequate workforce skills and training, which includes lack of adequate scientific, technical, and manufacturing skills required for renewable energy production; lack of reliable installation, maintenance, and inspection services; and failure of the educational system to provide adequate training in new technologies.

- Lack of adequate codes, standards, utility interconnection, and net-metering guidelines.

- Poor public perception of renewable energy system aesthetics.

- Lack of stakeholder/community participation and co-operation in energy choices and renewable energy projects.

With such a wide range of non-technical barriers, there is no "silver bullet" solution to drive the transition to renewable energy. So ideally there is a need for several different types of policy instruments to complement each other and overcome different types of barriers.[71][74]

A policy framework must be created that will level the playing field and redress the imbalance of traditional approaches associated with fossil fuels. The policy landscape must keep pace with broad trends within the energy sector, as well as reflecting specific social, economic and environmental priorities.[75]

Public policy landscape

Public policy has a role to play in renewable energy commercialization because the free market system has some fundamental limitations. As the Stern Review points out:

In a liberalised energy market, investors, operators and consumers should face the full cost of their decisions. But this is not the case in many economies or energy sectors. Many policies distort the market in favour of existing fossil fuel technologies.[72]

The International Solar Energy Society has stated that "historical incentives for the conventional energy resources continue even today to bias markets by burying many of the real societal costs of their use".[76]

Lester Brown goes further and suggests that the market "does not incorporate the indirect costs of providing goods or services into prices, it does not value nature’s services adequately, and it does not respect the sustainable-yield thresholds of natural systems".[77] It also favors the near term over the long term, thereby showing limited concern for future generations.[77] Tax and subsidy shifting can help overcome these problems.[78]

Shifting taxes

Tax shifting involves lowering income taxes while raising levies on environmentally destructive activities, in order to create a more responsive market. It has been widely discussed and endorsed by economists. For example, a tax on coal that included the increased health care costs associated with breathing polluted air, the costs of acid rain damage, and the costs of climate disruption would encourage investment in renewable technologies. Several Western European countries are already shifting taxes in a process known there as environmental tax reform, to achieve environmental goals.[77]

A four-year plan adopted in Germany in 1999 gradually shifted taxes from labor to energy and, by 2001, this plan had lowered fuel use by 5 percent. It had also increased growth in the renewable energy sector, creating some 45,400 jobs by 2003 in the wind industry alone, a number that is projected to rise to 103,000 by 2010. In 2001, Sweden launched a new 10-year environmental tax shift designed to convert 30 billion kroner ($3.9 billion) of taxes on income to taxes on environmentally destructive activities. Other European countries with significant tax reform efforts are France, Italy, Norway, Spain, and the United Kingdom. Asia’s two leading economies, Japan and China, are considering the adoption of carbon taxes.[77]

Shifting subsidies

Subsidies are not inherently bad as many technologies and industries emerged through government subsidy schemes. The Stern Review explains that of 20 key innovations from the past 30 years, only one of the 14 they could source was funded entirely by the private sector and nine were totally funded by the public sector.[79] In terms of specific examples, the Internet was the result of publicly funded links among computers in government laboratories and research institutes. And the combination of the federal tax deduction and a robust state tax deduction in California helped to create the modern wind power industry.[78]

But just as there is a need for tax shifting, there is also a need for subsidy shifting. Lester Brown has argued that "a world facing the prospect of economically disruptive climate change can no longer justify subsidies to expand the burning of coal and oil. Shifting these subsidies to the development of climate-benign energy sources such as wind, solar, biomass, and geothermal power is the key to stabilizing the earth’s climate."[78] The International Solar Energy Society advocates "leveling the playing field" by redressing the continuing inequities in public subsidies of energy technologies and R&D, in which the fossil fuel and nuclear power receive the largest share of financial support.[80]

Some countries are eliminating or reducing climate disrupting subsidies and Belgium, France, and Japan have phased out all subsidies for coal. Germany reduced its coal subsidy from $5.4 billion in 1989 to $2.8 billion in 2002, and in the process lowered its coal use by 46 percent. Germany plans to phase out this support entirely by 2010. China cut its coal subsidy from $750 million in 1993 to $240 million in 1995 and more recently has imposed a tax on high-sulfur coals.[78]

While some leading industrial countries have been reducing subsidies to fossil fuels, most notably coal, the United States has been increasing its support for the fossil fuel and nuclear industries.[78]

Renewable energy targets

Setting national renewable energy targets can be an important part of a renewable energy policy and these targets are usually defined as a percentage of the primary energy and/or electricity generation mix. For example, the European Union has prescribed an indicative renewable energy target of 12 per cent of the total EU energy mix and 22 per cent of electricity consumption by 2010. National targets for individual EU Member States have also been set to meet the overall target. Other developed countries with defined national or regional targets include Australia, Canada, Japan, New Zealand, Norway, Switzerland, and some US States.[81]

National targets are also an important component of renewable energy strategies in some developing countries. Developing countries with renewable energy targets include China, India, Korea, Indonesia, Malaysia, the Philippines, Singapore, Thailand, Brazil, Israel, Egypt, Mali, and South Africa. The targets set by many developing countries are quite modest when compared with those in some industrialized countries.[81]

Renewable energy targets in most countries are indicative and nonbinding but they have assisted government actions and regulatory frameworks. The United Nations Environment Program has suggested that making renewable energy targets legally binding could be an important policy tool to achieve higher renewable energy market penetration.[81]

Green stimulus programs

In response to the global financial crisis, the world’s major governments have made “green stimulus” programs one of their main policy instruments for supporting the economic recovery. Some $188 billion in green stimulus funding had been allocated to renewable energy and energy efficiency. Most of the overall clean energy stimuli are expected to be spent in 2010 and in 2011.[82]

Employment

Current employment in the renewable energy sector and supplier industries is estimated at 2.3 million worldwide. The wind power industry employs some 300,000 people, the photovoltaics sector an estimated 170,000, and the solar thermal industry more than 600,000. Over 1 million jobs are found in the biofuels industry, associated with growing and processing a variety of feedstocks into ethanol and biodiesel.[83]

Recent developments

A number of events in 2006 pushed renewable energy up the political agenda, including the US mid-term elections in November, which confirmed clean energy as a mainstream issue. Also in 2006, the Stern Review[10] made a strong economic case for investing in low carbon technologies now, and argued that economic growth need not be incompatible with cutting energy consumption.[85] According to a trend analysis from the United Nations Environment Programme, climate change concerns[9] coupled with recent high oil prices[86] and increasing government support are driving increasing rates of investment in the renewable energy and energy efficiency industries.[11][13]

Investment capital flowing into renewable energy reached a record US$77 billion in 2007, with the upward trend continuing in 2008.[12] The OECD still dominates, but there is now increasing activity from companies in China, India and Brazil. Chinese companies were the second largest recipient of venture capital in 2006 after the United States. In the same year, India was the largest net buyer of companies abroad, mainly in the more established European markets.[13]

Global revenues for solar photovoltaics, wind power, and biofuels expanded from $75.8 billion in 2007 to $115.9 billion in 2008. For the first time, one sector alone, wind, had revenues exceeding $50 billion. New global investments in clean energy technologies — including venture capital, project finance, public markets, and research and development — expanded by 4.7 percent from $148.4 billion in 2007 to $155.4 billion in 2008.[17]

Continued growth for the renewable energy sector is expected in the mid- to long-term, but 2009 will be a year of refocus, consolidation, or retrenchment for many companies. At the same time, new government spending, regulation, and policies should help the industry weather the current economic crisis better than many other sectors.[17] Most notably, U.S. President Barack Obama's American Recovery and Reinvestment Act of 2009 includes more than $70 billion in direct spending and tax credits for clean energy and associated transportation programs. This policy-stimulus combination represents the largest federal commitment in U.S. history for renewables, advanced transportation, and energy conservation initiatives. Based on these new rules, many more utilities are expected to strengthen their clean-energy programs.[17]

Clean Edge suggests that the commercialization of clean energy will help countries around the world pull out of the current economic malaise.[17]

Sustainable energy

Moving towards energy sustainability will require changes not only in the way energy is supplied, but in the way it is used, and reducing the amount of energy required to deliver various goods or services is essential. Opportunities for improvement on the demand side of the energy equation are as rich and diverse as those on the supply side, and often offer significant economic benefits.[87]

Renewable energy and energy efficiency are said to be the “twin pillars” of sustainable energy policy. Any serious vision of a sustainable energy economy requires commitments to both renewables and efficiency. The American Council for an Energy-Efficient Economy has explained that both resources must be developed in order to stabilize and reduce carbon dioxide emissions:[88]

Efficiency is essential to slowing the energy demand growth so that rising clean energy supplies can make deep cuts in fossil fuel use. If energy use grows too fast, renewable energy development will chase a receding target. Likewise, unless clean energy supplies come online rapidly, slowing demand growth will only begin to reduce total emissions; reducing the carbon content of energy sources is also needed.[88]

The IEA has stated that renewable energy and energy efficiency policies should be viewed as complementary tools for the development of a sustainable energy future, instead of being developed in isolation.[89]

See also

Lists

- List of large wind farms

- List of notable renewable energy organizations

- List of renewable energy topics by country

Topics

- Clean Energy Trends

- Ecotax

- Energy security and renewable technology

- Feed-in Tariff

- International Renewable Energy Agency

- PV financial incentives

- Rocky Mountain Institute

- Relative cost of electricity generated by different sources

- The Clean Tech Revolution

- World Council for Renewable Energy

People

|

|

|

Categories

- Category:Renewable energy by country

- Category:Renewable energy commercialization

References

- ↑ REN21 (2008). Renewables 2007 Global Status Report (Paris: REN21 Secretariat and Washington, DC: Worldwatch Institute).

- ↑ 2.00 2.01 2.02 2.03 2.04 2.05 2.06 2.07 2.08 2.09 2.10 2.11 International Energy Agency (2007). Renewables in global energy supply: An IEA facts sheet (PDF) OECD, 34 pages.

- ↑ International Council for Science (c2006). Discussion Paper by the Scientific and Technological Community for the 14th session of the United Nations Commission on Sustainable Development (CSD-14) (PDF)

- ↑ 4.0 4.1 4.2 National Renewable Energy Laboratory (2006). Nontechnical Barriers to Solar Energy Use: Review of Recent Literature, Technical Report, NREL/TP-520-40116, September, 30 pages.

- ↑ 5.0 5.1 5.2 5.3 International Energy Agency. IEA urges governments to adopt effective policies based on key design principles to accelerate the exploitation of the large potential for renewable energy 29 September 2008.

- ↑ Donald W. Aitken. Transitioning to a Renewable Energy Future, International Solar Energy Society, January 2010, p. 3.

- ↑ 7.0 7.1 7.2 REN21 (2010). Renewables 2010 Global Status Report p. 13.

- ↑ 8.0 8.1 REN21 (2009). Renewables Global Status Report: 2009 Update p. 17.

- ↑ 9.0 9.1 9.2 REN21 (2006). Changing climates: The Role of Renewable Energy in a Carbon-constrained World (PDF) p. 2.

- ↑ 10.0 10.1 HM Treasury (2006). Stern Review on the Economics of Climate Change.

- ↑ 11.0 11.1 New UN report points to power of renewable energy to mitigate carbon emissions UN News Centre, 8 December 2007.

- ↑ 12.0 12.1 Joel Makower, Ron Pernick and Clint Wilder (2008). Clean Energy Trends 2008, Clean Edge, p. 2.

- ↑ 13.0 13.1 13.2 United Nations Environment Programme and New Energy Finance Ltd. (2007). Global Trends in Sustainable Energy Investment 2007: Analysis of Trends and Issues in the Financing of Renewable Energy and Energy Efficiency in OECD and Developing Countries (PDF) p. 3.

- ↑ Top of the list, Renewable Energy World, 2 January 2006.

- ↑ 15.0 15.1 15.2 Mark Osborne, First Solar’s market share set to soar, PV-Tech.org, September 7th 2009, accessed on January 7th 2010.

- ↑ 16.0 16.1 16.2 16.3 16.4 Keith Johnson, Wind Shear: GE Wins, Vestas Loses in Wind-Power Market Race, Wall Street Journal, March 25th 2009, accessed on January 7th 2010.

- ↑ 17.0 17.1 17.2 17.3 17.4 17.5 17.6 17.7 Joel Makower, Ron Pernick and Clint Wilder (2009). Clean Energy Trends 2009, Clean Edge, pp. 1-4.

- ↑ REN21 (2010). Renewables 2010 Global Status Report p. 9 & 34.

- ↑ Lester R. Brown. Plan B 4.0: Mobilizing to Save Civilization, Earth Policy Institute, 2009, p. 135.

- ↑ 20.0 20.1 REN21 (2010). Renewables 2010 Global Status Report p. 15.

- ↑ REN21 (2009). Renewables Global Status Report: 2009 Update p. 9.

- ↑ 22.0 22.1 Eric Martinot and Janet Sawin. Renewables Global Status Report 2009 Update, Renewable Energy World, September 9, 2009.

- ↑ Americans Willing To Pay More for Solar Renewable Energy World, 25 June 2010.

- ↑ Donald W. Aitken. Transitioning to a Renewable Energy Future, International Solar Energy Society, January 2010, p. 3.

- ↑ Renewable energy costs drop in '09 Reuters, November 23, 2009.

- ↑ Solar Power 50% Cheaper By Year End - Analysis Reuters, November 24, 2009.

- ↑ 27.0 27.1 Al Gore (2009). Our Choice, Bloomsbury, p. 58.

- ↑ Mark Z. Jacobson (2009). Review of Solutions to Global Warming, Air Pollution, and Energy Security p. 5.

- ↑ Duncan Graham-Rowe. Hydroelectric power's dirty secret revealed New Scientist, 24 February 2005.

- ↑ Bertani, R., 2003, "What is Geothermal Potential?", IGA News, 53, page 1-3.

- ↑ 31.0 31.1 31.2 Fridleifsson, I.B., R. Bertani, E. Huenges, J. W. Lund, A. Ragnarsson, and L. Rybach (2008). The possible role and contribution of geothermal energy to the mitigation of climate change. In: O. Hohmeyer and T. Trittin (Eds.), IPCC Scoping Meeting on Renewable Energy Sources, Proceedings, Luebeck, Germany, 20–25 January 2008, p. 59-80.

- ↑ Islandsbanki Geothermal Research, United States Geothermal Energy Market Report, October 2009, accessed through website of Islandbanki.

- ↑ Leonora Walet. Philippines targets $2.5 billion geothermal development, Reuters, November 5, 2009.

- ↑ 34.0 34.1 REN21 (2009). Renewables Global Status Report: 2009 Update pp. 12-13.

- ↑ International Energy Agency. Solar assisted air-conditioning of buildings

- ↑ Lester R. Brown. Plan B 4.0: Mobilizing to Save Civilization, Earth Policy Institute, 2009, p. 122.

- ↑ Greenpeace Energy (2008). World's largest photovoltaic power plants

- ↑ LCG Consulting. FPL Commissions DeSoto Next Generation Solar Energy Center Energy Online, October 28, 2009.

- ↑ Earth Policy Institute (2007). Solar Cell Production Jumps 50 Percent in 2007 Retrieved on 3 December 2008.

- ↑ "Stabilizing Climate" (PDF) in Lester R. Brown, Plan B 2.0 Rescuing a Planet Under Stress and a Civilization in Trouble (NY: W.W. Norton & Co., 2006), p. 189.

- ↑ Clean Edge (2007). The Clean Tech Revolution... the costs of clean energy are declining (PDF) p.8.

- ↑ Lars Kroldrup. Gains in Global Wind Capacity Reported Green Inc., February 15, 2010.

- ↑ World Wind Energy Association (2008). Wind turbines generate more than 1 % of the global electricity

- ↑ Global wind energy markets continue to boom – 2006 another record year (PDF).

- ↑ Global Wind Energy Council (2009). Global Wind 2008 Report, p. 9. Retrieved January 4, 2010.

- ↑ International Energy Agency (2009). IEA Wind Energy: Annual Report 2008 p. 9.

- ↑ 47.0 47.1 REN21 (2008). Renewables 2007 Global Status Report (PDF) p. 12.

- ↑ United Nations Environment Programme (2009). Assessing Biofuels, p.15.

- ↑ America and Brazil Intersect on Ethanol Renewable Energy Access, 15 May 2006.

- ↑ New Rig Brings Brazil Oil Self-Sufficiency Washington Post, 21 April 2006.

- ↑ Erica Gies. As Ethanol Booms, Critics Warn of Environmental Effect The New York Times, June 24, 2010.

- ↑ 52.0 52.1 52.2 Worldwatch Institute and Center for American Progress (2006). American energy: The renewable path to energy security (PDF)

- ↑ International Energy Agency (2006). World Energy Outlook 2006 (PDF).

- ↑ Biotechnology Industry Organization (2007). Industrial Biotechnology Is Revolutionizing the Production of Ethanol Transportation Fuel pp. 3-4.

- ↑ Decker, Jeff. Going Against the Grain: Ethanol from Lignocellulosics, Renewable Energy World, January 22, 2009.

- ↑ "Building Cellulose" (PDF). http://www.grainnet.com/pdf/cellulosemap.pdf. Retrieved 2010-07-08.

- ↑ Range Fuels receives $80 million loan

- ↑ 58.0 58.1 Jeff Scruggs and Paul Jacob. Harvesting Ocean Wave Energy, Science, Vol. 323, 27 February 2009, p. 1176.

- ↑ Orkney to get 'biggest' wave farm BBC News, 20 February 2007.

- ↑ World tidal energy first for NI, BBC News BBC News, 7 June 2007.

- ↑ Bertani, Ruggero (2009), ""Geothermal Energy: An Overview on Resources and Potential"", International Geothermal Days, Slovakia

- ↑ "Profits soar for top wind turbine maker". Edie.net. 2007-03-21. http://www.edie.net/news/news_story.asp?id=12798&channel=0. Retrieved 2010-07-08.

- ↑ "Vestas History". Vestas.com. 2009-02-27. http://www.vestas.com/en/about-vestas/history. Retrieved 2010-07-08.

- ↑ "Portfolio 21: Vestas Wind Systems Top Green Company of 2006". Environmentalleader.com. 2007-01-29. http://www.environmentalleader.com/2007/01/29/portfolio-21-vestas-wind-systems-top-green-company-of-2006/. Retrieved 2010-07-08.

- ↑ "Wind-Power Co. Plans To Expand In Portland". KPTV. 2008-12-01. http://www.kptv.com/money/18180440/detail.html.

- ↑ GE Energy (undated). GE Energy Retrieved on 22 January 2008.

- ↑ Nuke Producer GE Energy Buys Solar Producer AstroPower Social Funds, 6 April 2004.

- ↑ 68.0 68.1 Benjamin K. Sovacool. “Rejecting Renewables: The Socio-technical Impediments to Renewable Electricity in the United States,” Energy Policy, 37(11) (November, 2009), p. 4500.

- ↑ Benjamin K. Sovacool. “The Cultural Barriers to Renewable Energy in the United States,” Technology in Society, 31(4) (November, 2009), p. 372.

- ↑ Mark Z. Jacobson and Mark A. Delucchi. A Path to Sustainable Energy by 2030, Scientific American, November 2009, p. 45.

- ↑ 71.0 71.1 71.2 United Nations Department of Economic and Social Affairs, (2005). Increasing Global Renewable Energy Market Share: Recent Trends and Perspectives Final Report.

- ↑ 72.0 72.1 HM Treasury (2006). Stern Review on the Economics of Climate Change p. 355.

- ↑ Matthew L. Wald. Fossil Fuels’ Hidden Cost Is in Billions, Study Says The New York Times, October 20, 2009.

- ↑ Diesendorf, Mark (2007). Greenhouse Solutions with Sustainable Energy, UNSW Press, p. 293.

- ↑ IEA Renewable Energy Working Party (2002). Renewable Energy... into the mainstream p. 48.

- ↑ Donald W. Aitken. Transitioning to a Renewable Energy Future, International Solar Energy Society, January 2010, p. 4.

- ↑ 77.0 77.1 77.2 77.3 Brown, L.R. (2006). Plan B 2.0 Rescuing a Planet Under Stress and a Civilization in Trouble W.W. Norton & Co, pp. 228-232.

- ↑ 78.0 78.1 78.2 78.3 78.4 Brown, L.R. (2006). Plan B 2.0 Rescuing a Planet Under Stress and a Civilization in Trouble W.W. Norton & Co, pp. 234-235.

- ↑ HM Treasury (2006). Stern Review on the Economics of Climate Change p. 362.

- ↑ Donald W. Aitken. Transitioning to a Renewable Energy Future, International Solar Energy Society, January 2010, p. 6.

- ↑ 81.0 81.1 81.2 United Nations Environment Program (2006). Changing climates: The Role of Renewable Energy in a Carbon-constrained World pp. 14-15.

- ↑ REN21 (2010). Renewables 2010 Global Status Report p. 27.

- ↑ "Green Jobs: Working for People and the Environment". Worldwatch.org. http://www.worldwatch.org/node/5925. Retrieved 2010-07-08.

- ↑ Makower, J. Pernick, R. Wilder, C. (2008). Clean Energy Trends 2008

- ↑ United Nations Environment Programme and New Energy Finance Ltd. (2007), p. 11.

- ↑ High oil price hits Wall St ABC News, 16 October 2007. Retrieved on 15 January 2008.

- ↑ InterAcademy Council (2007). Lighting the way: Toward a sustainable energy future

- ↑ 88.0 88.1 American Council for an Energy-Efficient Economy (2007). The Twin Pillars of Sustainable Energy: Synergies between Energy Efficiency and Renewable Energy Technology and Policy Report E074.

- ↑ International Energy Agency (2007). Global Best Practice in Renewable Energy Policy Making

Bibliography

- Aitken, Donald W. (2010). Transitioning to a Renewable Energy Future, International Solar Energy Society, January, 54 pages.

- HM Treasury (2006). Stern Review on the Economics of Climate Change, 575 pages.

- International Council for Science (c2006). Discussion Paper by the Scientific and Technological Community for the 14th session of the United Nations Commission on Sustainable Development, 17 pages.

- International Energy Agency (2006). World Energy Outlook 2006: Summary and Conclusions, OECD, 11 pages.

- International Energy Agency (2007). Renewables in global energy supply: An IEA facts sheet, OECD, 34 pages.

- International Energy Agency (2008). Deploying Renewables: Principles for Effective Policies, OECD, 8 pages.

- Makower, Joel, and Ron Pernick and Clint Wilder (2009). Clean Energy Trends 2009, Clean Edge.

- National Renewable Energy Laboratory (2006). Non-technical Barriers to Solar Energy Use: Review of Recent Literature, Technical Report, NREL/TP-520-40116, September, 30 pages.

- REN21 (2008). Renewables 2007 Global Status Report, Paris: REN21 Secretariat, 51 pages.

- REN21 (2009). Renewables Global Status Report: 2009 Update, Paris: REN21 Secretariat.

- REN21 (2010). Renewables 2010 Global Status Report, Paris: REN21 Secretariat, 78 pages.

- United Nations Environment Programme and New Energy Finance Ltd. (2007). Global Trends in Sustainable Energy Investment 2007: Analysis of Trends and Issues in the Financing of Renewable Energy and Energy Efficiency in OECD and Developing Countries, 52 pages.

- Worldwatch Institute and Center for American Progress (2006). American energy: The renewable path to energy security, 40 pages.

External links

- Global Renewable Energy: Policies and Measures

- Missing the Market Meltdown

- Renewable Energy Tops 10% of U.S. Energy Production

- Half of Global Electricity To Come From Renewables IEA Says

- Renewable Energy Potentials

- Optimism Abounds Throughout Renewable Energy Industry

- GE Energy turbine sales to grow fivefold in Europe

- New renewables to power 40 percent of global electricity demand by 2050

|

||||||||||||||||||||||

|

|||||

|

|||||||||||||||||||

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||